If you own a business, it's important for you to understand the basics of payment processing. You want to be able to receive payments smoothly, but it's not just about that.

You're responsible for your customers' private financial information as soon as they enter their payment details on your site, so you want to be as informed as possible about the process in case any issues ever come up.

I'm going to explain exactly what happens behind the scenes when a customer makes a purchase, to give you a good understanding of the full picture. I'll also tell you about the best ways to accept payments on your website.

What Is Payment Processing and Why Do You Need It?

Payment processing is a general term used to describe the sequence of processes that take place behind the scenes of electronic transactions. These transactions can be via credit card, debit card, digital wallet, or any other digital payment method.

If you want to sell on your own website, whether you're selling goods, services, or subscriptions, you'll need a way to accept credit cards and other payment methods. You'll need the infrastructure to allow smooth and secure transactions.

Accepting online payments can be risky. There's always the possibility that a card is stolen or counterfeit. Cybercriminals are lurking everywhere, looking for opportunities to turn a profit by taking advantage of unsuspecting merchants.

A payment processor can take care of all of this for you. When someone pays you with a credit card, the processor verifies the authenticity of the card and handles all communication between any involved banks and credit card companies.

How Does Payment Processing Work?

Payment processing happens in 3 steps: authorization, authentication, and settlement. Let's take a closer look at each one.

Authorization

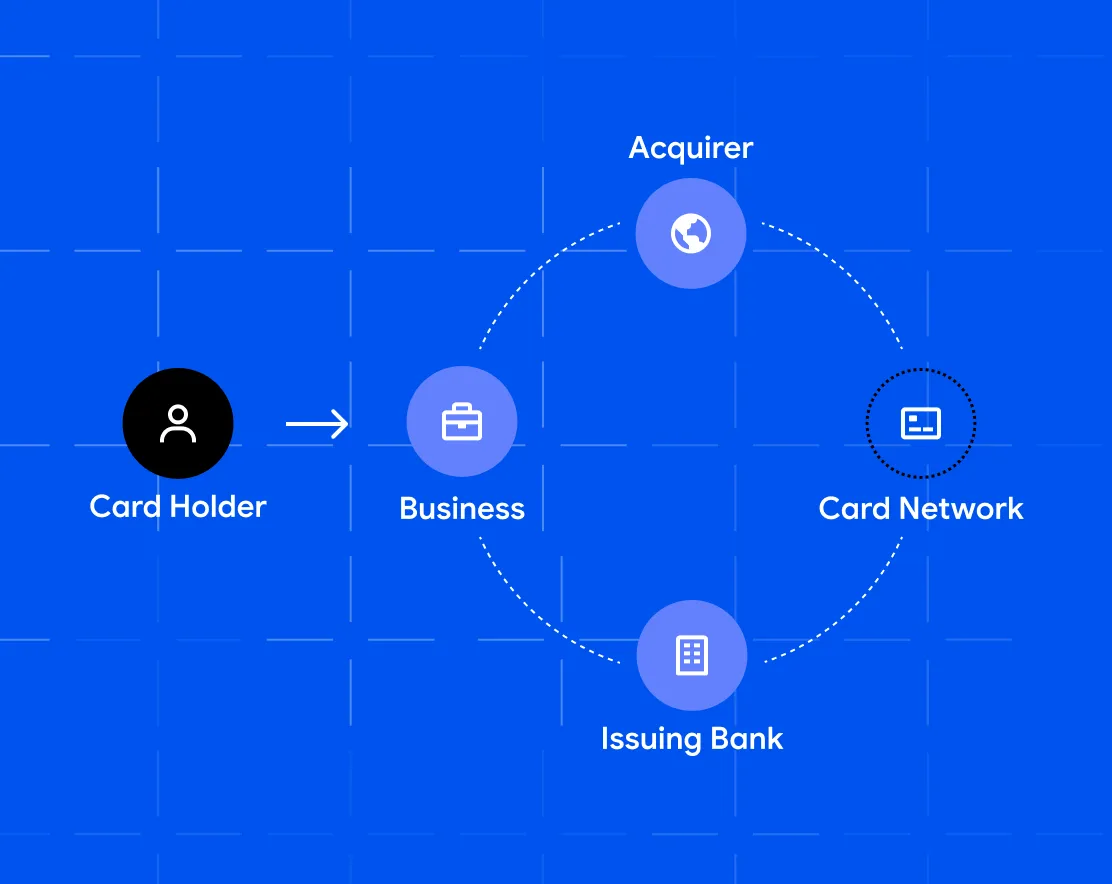

For a credit or debit card transaction to go through successfully, the card details must be verified and authorized. This step ensures that the customer's card is valid and legitimate. Here's how it works:

- The customer enters their card information on a website checkout page or inserts their card into a POS terminal at a brick-and-mortar business.

- The card details are encrypted and sent to the acquiring bank (the seller's bank).

- The acquiring bank sends the card details to the credit card association (e.g. Visa, Mastercard, or American Express).

- The credit card association approves the payment request and asks the issuing bank (the customer's bank) to authorize the transaction.

- The issuing bank authorizes the transaction once it verifies the card number, expiration date, security code, billing address and total payment amount.

During this process, it is the payment processor that handles the communication, asking the banks and card associations for authorization. Although this sounds like a lot of steps, it generally only takes a few moments to complete.

Authentication

Once the issuing bank is satisfied that the card details are verified, it authenticates the purchase so the payment can be released to the acquiring bank. Here's what happens during this stage:

- The issuing bank gives the credit card association its approval.

- The credit card association passes on the authorization to the acquiring bank.

- The issuing bank puts a temporary hold on the customer's account in the amount of the purchase. Once the transaction clears, these funds will be withdrawn and deposited in the seller's account.

- The customer sees a confirmation message on the checkout page or receives a hard copy receipt in a brick-and-mortar business.

If the issuing bank does not approve the transaction for any reason, it will notify the card association and acquiring bank and the transaction will be canceled. The customer will see an error message, usually explaining the reason for the rejection.

Settlement

In the final stage of payment processing, the issuing bank releases the funds and they are transferred to the seller's account in the acquiring bank. It can take a few days for the transaction to settle and for the seller to see the funds. Here's what's going on in the background:

- At the end of each day, all approved authorizations from the day are sent to the acquiring bank.

- The acquiring bank passes this information on to the credit card association.

- The credit card association works to settle each individual transaction, which involves getting the funds to the seller, removing the hold from the customer's account, and finalizing the transaction.

- The credit card association sends the issuing bank notice of all approved transactions.

- The issuing bank transfers the funds to the credit card association.

- The credit card association passes the funds on to the acquiring bank.

- The acquiring bank deposits the funds in the seller's account.

- The issuing bank deducts the funds from the customer's account and closes the transaction.

How You Can Optimize Your Payment System to Grow Your Revenue

The best businesses are always looking for ways to enhance their revenue growth. Here are a few key ways to optimize your payment system to increase your number of sales.

Speed Up the Checkout Process

Today's online shoppers expect a sub-10-second checkout experience. With digital wallets capturing 53% of all global online purchases and modern consumers expecting frictionless payments, speed is essential.

With Pay.com, you can securely store your customers' details and payment preferences so returning customers don't have to reenter all their information. This way, you can create a faster online payment process, reduce cart abandonment, and increase your conversion rates.

Make Sure Your Checkout Process Is Mobile-Friendly

Mobile commerce continues to surge globally. With billions of consumers using digital wallets on their phones, it's critical to make sure your checkout works smoothly on smaller screens. It's also a good idea to accept mobile-friendly payment methods such as Google Pay and Apple Pay.

Put an Emphasis on Security

With cybercrime on the rise, it's becoming increasingly important for consumers to feel safe when paying for something online. In fact, a lack of visible security is one of the leading causes of cart abandonment.

Pay.com uses the 3D Secure protocol that provides an additional layer of security. You can show the 3D Secure symbol and other security logos throughout your checkout process to increase trust and confidence.

Provide a Range of Payment Options

Offering local payment options is an excellent way to build trust with customers and increase your sales. Digital wallets now represent 60%+ of the global population with 5.2 billion users worldwide. Beyond digital wallets, BNPL (Buy Now, Pay Later) services have grown to $28.44 billion in annual revenues, while A2A (Account-to-Account) payments hit $1.4 trillion in consumer transactions in 2026.

Pay.com lets you accept a wide range of payment methods on your website, from traditional cards to cutting-edge digital solutions.

Payment Processing Terminology

As a business owner, it's a good idea to be familiar with the key terms involved in payment processing:

- Credit card processing: A system that enables credit card data to be transmitted through an electronic card network. The system validates and approves transactions and transfers funds between accounts.

- Debit card processing: Similar to credit card processing, but less complex, and typically takes place on different networks. As a merchant, you can usually accept both credit and debit cards using the same software (and hardware, if applicable).

- ACH transfers: Automated Clearing House (ACH) is a network run by the National Automated Clearing House Association (NACHA). It enables the routing of payments between banks and can be used for money transfers, recurring payments to pay back debt, paycheck deposit, and more.

- Mobile payment systems: Also known as mobile or digital wallets, these platforms allow users to make payments on their mobile devices without having to enter their credit card details each time. Examples include Google Pay, Apple Pay, and digital wallet solutions.

- Payment processor: A company that enables merchants to accept payments and processes those payments for them.

- Payment gateway: Basically, an online version of a point-of-sale (POS) terminal. It's a front-end software application on a merchant's website that enables online payments. Payment gateways capture and send credit card data to the payment processor and communicate approvals or rejections.

- POS (Point of Sale) terminal: A system consisting of hardware and software that enables brick-and-mortar merchants to accept credit and debit transactions. The hardware usually includes a computer and several connected devices, such as card readers and receipt printers.

- Merchant bank (acquirer): A financial institution a merchant can use to accept customers' debit and credit card payments.

- Card issuer: A financial institution that provides credit and debit cards on behalf of card networks such as Visa, Mastercard, and American Express.

- Credit card network: A company that facilitates the connectivity between the merchant bank and the card issuers. There are four main card networks: Visa, Mastercard, Discover, and American Express.

- Address Verification System (AVS): A service provided by credit card networks to verify whether a cardholder's official billing address in the card issuer's system matches the billing information entered by the customer. This process helps reduce online payment fraud and chargebacks.

How to Protect Yourself from Fraud

Every day, billions of dollars are processed around the world. While most transactions run smoothly, there are some potential issues to be aware of. The biggest issue is fraud, which can end up costing you huge amounts of money.

There are a few steps you can take to mitigate the risk.

- Choose a payment processor that offers PCI-compliant data security and protection, such as Pay.com. You don't need to be a cybersecurity expert, but you definitely want to be sure that your payment processor is using all the latest protections.

- Require your customers to provide their billing address, card expiration date, and CVV (card verification value) code. The more data you ask for, the less opportunity there is for fraudulent behavior.

- Use SSL (secure sockets layer) certificates and other security measures like 3DS2 to protect the safety of all transactions on your online store. Most payment processors will require the use of SSL certificates for any ecommerce merchant that they work with.

- Make sure all of the hardware and software that you use is up to date and that all of the latest patches and security updates are installed.

The Bottom Line: How to Choose a Payment Processor

It's important to do your research to find the best payment processor for your business. You'll want to make sure the service you choose can help you accept a variety of payment methods in addition to credit cards and debit cards.

As discussed above, security is extremely important when it comes to online transactions, so always go with a PCI-compliant payment processor. Ask questions about the fraud prevention elements your processor has in place.

Pay.com provides a complete payment infrastructure that allows you to accept payments on your website. It's easy to set up and get started, even if this is your first time selling online. It comes with the latest security features and fraud protection technology, giving you peace of mind.

FAQs

How long does it take to process a payment?

The actual payment processing time is very quick - a few seconds or minutes at most. However, the time it takes for the transaction to settle and for the seller to actually receive the funds can take up to 3-5 business days, depending on the payment method.

Does processed mean paid?

Processed does not necessarily mean paid. If the bank says a transaction has been processed, that can mean that it has been authorized and authenticated but not yet settled - meaning, the seller may not see the funds in their account yet.

How secure is payment processing?

Whenever someone pays with a credit or debit card, there is a risk of identity theft or other types of fraud. The card could be stolen or private financial and identifying information could be stolen while the card is being processed. Fortunately, there are plenty of protections that payment processors use to ensure the security of transactions. When you choose a secure payment infrastructure like Pay.com, all the data is encrypted and sent through secure channels.

Why are card transactions denied?

There are several reasons why a transaction may be denied. In many cases, it's as simple as a typo in the card details. In other cases, the payment processor does not accept that particular type of card, there are insufficient funds in the account, additional verification is needed, or a technical error interrupted the payment process.

How do I decide which payment processor to use?

Choosing the right payment processor for your business can be a challenge. Once you have a good idea of what you need, your top considerations should include flexibility, ease of use, the ability to accept a wide range of payment methods, and security features.

Will my business qualify for a merchant account?

It depends. If you've experienced past bankruptcies or have a bad credit report, you may struggle to get approved. However, if there are no significant problems with your credit history and you can provide all the required information, you should have no issues opening a merchant account.

How much does payment processing cost?

Generally, credit card processing fees will cost your business between 1.5 and 3.5% of each transaction. It's a good idea to choose a payment services provider which is completely transparent about its fees.

Pay.com lets you accept a variety of payment methods on your website and provides a full payment infrastructure to cover all your needs. It’s easy to set up and you don’t need any technical experience.

Emily is a content writer with a special interest in fintech and business. She loves sharing her knowledge to help small businesses take their first steps towards success.

Read next

Get payments insights in your inbox