What’s a Chargeback? How Can It Affect Your Business? [2026]

10 min read

•

17 Apr 2026

Chargebacks are an unfortunate but necessary reality of doing business online. On the one hand, chargebacks hold you, the merchant, to a higher standard and help protect consumers from fraudulent charges. However, on the other hand, chargebacks also come at a severe cost, leading to lost merchandise and seriously impacting your profits. They can also lead to your merchant account getting shut down, terminating your ability to accept payments.

At Pay.com, we realize the subject of chargebacks can be confusing, as many factors have to be taken into account. That said, understanding what chargebacks are, why they occur, and how they work is vital for every business owner, let alone merchants who rely on card payments. This post will cover everything you need to know about chargebacks, so you can take the proper steps to prevent and dispute them.

What is a chargeback?

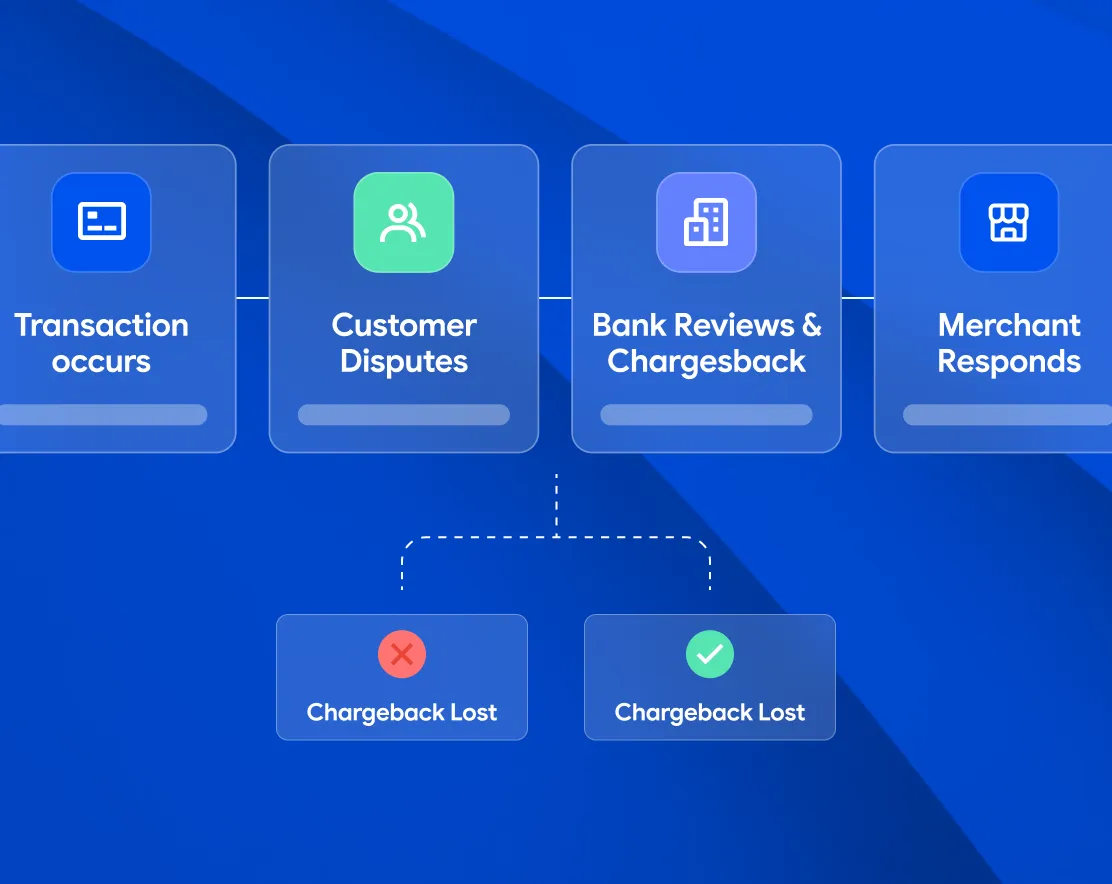

A chargeback is an act initiated by a cardholder to dispute a debit or credit card payment they believe to be illegitimate. When a chargeback occurs, a forced reimbursement of a transaction is initiated by the card issuer. Chargebacks can happen at any time after a sale occurs: however, they are most common within the first 120 days.

.webp)

How does a chargeback work?

The chargeback request process is set and managed by card networks and must be followed by financial institutions and merchants. The parties involved in the chargeback process include:

- The cardholder

- Issuing bank

- Acquiring bank

- Card Network

- Merchant

The chargeback process differs slightly depending on the card network. However, the general process looks something like this:

- The cardholder notifies their bank of a transaction they would like to dispute.

- The cardholder’s bank reviews the cardholder’s claim.

- If valid, the issuing bank sends the claim to the merchant’s bank.

- The acquiring bank notifies the merchant about the claim. It also informs the merchant that the transaction amount has been debited from their account to reimburse the cardholder.

- If the merchant wishes to fight the chargeback, they are provided forms to fill out and return within 7-10 days to explain their side of the dispute.

- The merchant then sends back the completed forms to the acquiring bank, which passes them onto the cardholder’s bank and sends the merchant a provisional credit for the chargeback amount.

- The issuing bank reviews the evidence submitted by the merchant. Merchants deemed to have fulfilled the transaction correctly keep the credit, while the cardholder’s credit gets withdrawn. If the issuing bank rules in favor of the cardholder, they will keep the credit, and the merchant’s credit is withdrawn.

.webp)

What causes chargebacks?

There are numerous reasons a customer might dispute a credit or debit card transaction. Unfortunately, not all of them are legitimate. Here are some of the most common:

- A cardholder was the victim of fraudulent transactions.

- A cardholder is overcharged for a product or service (billing error).

- A merchant failed to deliver the goods or services.

- A merchant misrepresented a product or service.

- A cardholder is not satisfied with a product or service.

- A cardholder is charged after a cancelled subscription service or fails to cancel a subscription service.

- A cardholder was accidentally charged twice for a purchase.

- A cardholder disputes a transaction for an illegitimate reason to keep goods or services without paying - aka Friendly fraud.

Difference between a chargeback and a payment dispute

Chargebacks and payment disputes are two standard terms often used interchangeably, even though they actually refer to two different, albeit similar things. A payment dispute occurs when a cardholder challenges a transaction on their credit card statement.

Disputes can arise for many reasons, but primarily stem from a customer viewing their credit card statement and believing that they did not make a purchase in the first place. Other common causes include incorrect transaction amounts and failure to deliver goods or services.

On the other hand, a chargeback is a forced reimbursement of a transaction initiated by the card issuer. So, a dispute is a process taken by a cardholder to contest a transaction. In contrast, a chargeback results from this process, but not all disputes end with a chargeback.

Chargeback Fees

A chargeback or dispute fee is a fee issued by acquiring banks to cover the administrative expenses incurred when processing a chargeback. When a customer’s card issuing bank processes a chargeback request or dispute, you as the merchant will very likely get charged a fee. How much this fee equates to depend on the bank, but generally ranges from $10 to $50. You could potentially pay much more if you’re considered a high-risk merchant.

In addition to the dispute fee, there are many associated expenses most merchants often don’t even think about. For example, payment processor fees are not returned when a chargeback occurs, so merchants must absorb that cost. All the operational costs that go into processing an order (warehouse management, logistics, transportation, etc.) also go to waste.

As you can see, chargeback fees can come with an extremely high cost. The good news is that there are a few ways to minimize your chances of getting impacted. These include confirming a cardholder’s identity, making your billing terms and conditions clear, and putting your shipping and return policies in an easily accessible place on your website.

How to handle chargebacks (step by step)

As a merchant, you should always be ready to respond to chargeback requests because they are bound to happen regularly. One of the most important things to handle chargebacks efficiently is staying organised and having good record-keeping practices. That way, if a customer disputes a charge on their card, you can be ready to fill out the required forms and respond as quickly as possible as soon as you’re notified of a claim.

Without good record-keeping practices or the authenticating information necessary at the time of purchase, handling chargebacks can become extremely cumbersome and time-consuming.

It’s also essential to know why the chargeback request occurred in the first place. To do this, you’ll need to understand the reason code, which is attached to the transaction by the issuing bank. However, as a merchant, you also need to understand that you can’t afford to simply accept chargebacks. You’ll need to defend any valid transactions and recover lost revenue, requiring you to follow the chargeback rep resentment process. Chargeback representment is a regulated process for responding to unwarranted chargebacks.

To successfully fight a chargeback, you’ll need to:

- Collect compelling evidence that is relevant based on the reason code provided and specific card scheme requirements. This can include things like a sales receipt, customer communications, and delivery confirmation.

- Devise a chargeback rebuttal letter that includes a summary of the evidence provided and an explanation of how you can prove that the transaction in question is valid.

- Submit the representment within the required timeline.

All of this can be done in-house if you have the resources and expertise to do so. If not, it’s advised to hire a third party that specialises in chargebacks. All merchants should also use a payment processor that provides protections against chargebacks. If you’re interested in how other merchants manage chargebacks, here are some interesting facts.

According to the 2021 Payment Risk Mitigation Survey by Worldpay and Forrester Consulting, in-house teams manage chargebacks for half of the merchants surveyed, with external teams managing chargebacks for 31% of global merchants surveyed. 18% report using a hybrid model that combines internal teams and third-party providers.

.webp)

How does a chargeback work on a credit card?

Credit card chargebacks are an excellent defense for cardholders and are often successful when filed. In fact, the credit card company chargeback process is now so easy that more and more merchants are reporting customers are using chargebacks in place of refunds. 80% of merchants surveyed have also reported experiencing an increase in friendly fraud attacks over the past three years.

The old-fashioned idea that chargebacks take a long time to process is a relic from a bygone era. In today's digital world, strict deadlines determine how long consumers, banks, and merchants have to initiate or respond to the chargeback process. These deadlines vary depending on the specific card network you're dealing with.

Visa card chargeback

- Cardholders have 120 days from the day after the transaction date to file a chargeback request for most issues.

- Merchants have 30 days to respond and fight a chargeback.

- Merchants have 10 days to file for arbitration.

Mastercard chargeback

- Cardholders have 120 days from the day of the transaction to file a chargeback for most issues.

- Merchants have 45 days to respond and fight a chargeback.

- Merchants have 45 days to file for arbitration.

American Express chargeback

- Cardholders have 120 days from the day of the transaction to file a chargeback for most issues.

- Merchants have 20 days to respond and fight a chargeback.

Merchant rights

While consumers have a powerful weapon to use in chargebacks, merchants are not defenseless. Merchants have rights within the chargeback process and can dispute chargebacks whenever they see fit. Even though fighting a chargeback request can take time and resources, it is a fundamental right that all merchants should utilise to recover lost revenue and defend themselves against dishonest customers. However, there are also some other vital rights every merchant should know about.

- The total for all chargebacks for a transaction cannot exceed the original purchase amount.

- If a customer files a chargeback claim for late delivery, they must first try to get a return. A chargeback is only possible if both the return and refund are denied.

- Returned items are not eligible for chargebacks until fifteen days after the return is received. This enables merchants to have enough time to issue a refund.

Debit card chargebacks

There are several critical differences between debit card chargebacks and credit card chargebacks. One of the most important is that debit card transactions take cash straight from a person’s bank account, while credit card payments simply record a debt. There is also a difference in the time it takes for a customer to receive a reimbursement.

Refunds usually take around 10 days to process debit cards, compared to 1-2 days for credit cards. However, if a debit card dispute happens to enter into the chargeback process, merchants will have to follow the same steps to fight a claim as they would when dealing with a credit card chargeback. Just like credit card chargebacks, debit card chargebacks are also something every merchant will have to confront.

The best way to prevent or reduce debit card chargebacks from occurring is to be proactive and clearly communicate. This means having a high level of customer service that enables customers to easily get in contact. Merchants should also share their return, exchange, and authorization policies with customers.

Visa card chargeback

When a Visa cardholder files a dispute, a transaction is turned into what is known as a Visa dispute. Visa disputes (aka chargebacks) are governed by rules set out by Visa. The chargeback process includes several steps.

- The issuing bank credits the cardholder’s account and notifies the merchant’s acquiring bank about the chargeback.

- The acquirer notifies the merchant and debits their account for the transaction amount, along with any chargeback fees.

- If a merchant wants to fight a claim, they must provide evidence to the issuing bank to prove the chargeback is illegitimate. If accepted, the chargeback is reversed.

Visa chargeback reason codes

Each chargeback claim is given a reason code, which helps explain to merchants the reason for the dispute. These codes fit into four categories:

(10) Fraud:

For transactions where no EMV chip was used, stolen payment card credentials were used or transactions were flagged by the Visa Fraud Program.

(11) Authorisation:

For transactions without the appropriate authorisation or where a Card Recovery Bulletin was ignored.

(12) Processing Errors:

For transactions with incorrect transaction codes, account numbers, and a range of other issues such as duplicate payments.

(13) Customer Disputes:

For transactions where services were not received, a product or service was not as advertised, or where a product is defective or counterfeit, among other reasons.

Mastercard chargeback

When a Mastercard holder files a dispute, the following chargeback process occurs according to rules set out by Mastercard. It should be noted that this process is different to Visa.

First Presentment:

This occurs when the transaction amount is taken from the cardholder and credited to the merchant account. If the cardholder wants to dispute the transaction, the issuing bank may ask for more information from the merchant.

- Chargeback:

The issuer will initiate a chargeback if the merchant fails to respond or provide compelling evidence that proves the transaction’s validity. If a chargeback occurs and the merchant does not choose to fight it, the total transaction amount is withdrawn from the merchant’s account and credited to the cardholder.

- Second Presentment:

Suppose a merchant chooses to fight the chargeback. In that case, they will need to provide evidence that proves the chargeback is invalid and send it to the acquirer. The acquirer can then process the second presentment if they believe the issuer’s chargeback didn’t meet the requirements of the chargeback reason code and can provide evidence that addresses the original reason for the dispute.

- Pre-arbitration (formerly Arbitration Chargeback):

The issuer needs to be convinced before reversing a chargeback. If not, the issuer moves the case to pre-arbitration. At this stage, the merchant can simply accept the or continue to fight the chargeback by presenting new evidence. The issuer then decides to reverse the chargeback or move to arbitration case filing.

- Arbitration Case Filing:

When an arbitration case is not resolved between the issuer and the acquirer (cardholder & merchant), Mastercard steps in to determine final responsibility for the dispute.

Mastercard chargeback reason codes

How can Pay help reduce chargeback disputes?

Pay.com enables merchants to increase conversions with a secure, fraud-resistant checkout that prevents certain fraud chargebacks and brings your business fully in line with the latest PSD2 legislation. With a 3D-secure component, our system decides how risky each transaction is based on the amount being spent and whether the shopper is known to your store.

Regular/familiar customers and those spending an expected amount are “exempted” from extra security measures. Only unfamiliar customers, large sums, and suspicious behavior is subject to more stringent checks. To find out more about how Pay.com helps protect you from fraud-based chargebacks - sign up now!

Learn more about our revenue optimizration & payment methods available for your eCommerce business. You can also begin to accept online payments today!

Related Content

Read next

Get payments insights in your inbox