What Are Cross-Border Payments? 2026 Guide for Businesses

9 min read

•

03 May 2026

Cross-border payments are international money transfers made between two parties in different countries. The term includes a range of transactions, including international remittance, foreign exchange, online payments, and more.

In this ultimate guide, I’ll walk you through all you need to know about cross-border payments so you can navigate the world of international payments with confidence and use them to your business’s advantage. I’ll explain what cross-border payments are, how they work and why they’re so important to your business.

{{text-box}}

What Are Cross-Border Payments?

Cross-border payments are international money transfers between two parties in two different countries. These payments are typically made between individuals and businesses or between businesses for commercial purposes. They involve the use of third-party providers, such as banks, payment processors, and money transfer services, to facilitate the transfer.

Cross-border payments can also involve multiple currencies, additional fees, exchange rates, and other considerations.

Cross-border payments can be made through a variety of methods, including wire transfers and credit and debit cards. Payment service providers or payment processors are commonly used to facilitate fast, reliable, and cost-effective ecommerce payments across borders.

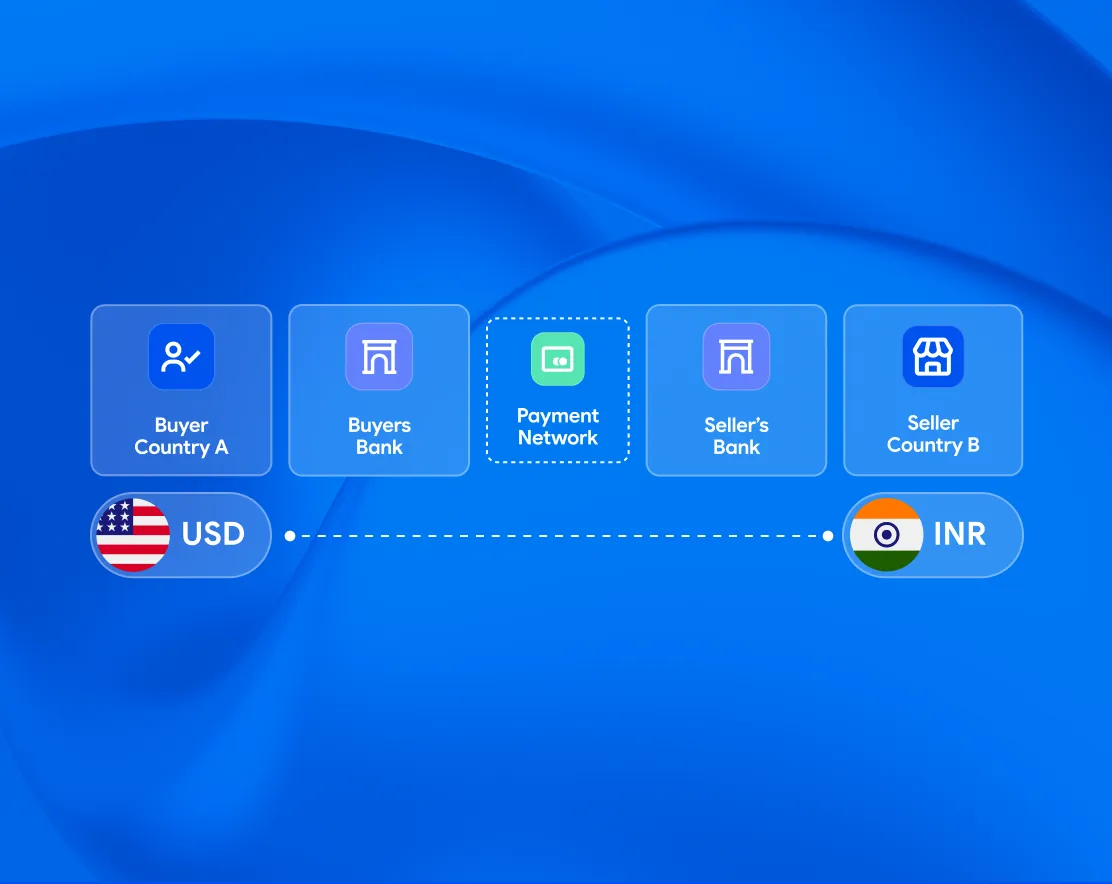

How Do Cross-Border Payments Work?

In a typical cross-border payment transaction, a sender initiates a payment by providing instructions to their bank in the originating country. The originating bank then sends a payment message to the recipient's bank in the destination country via a secure payments network.

The payment message contains details of the payment, including the payment amount and currency, the sender's and recipient's details, and the payment instructions.

The originating bank also informs the recipient's bank of the payment amount and the currency it is denominated in. The recipient's bank then debits the sender's account and converts the payment amount into its own local currency. The funds are then transferred to the recipient's account. The recipient's bank may also provide the recipient with a confirmation of the payment.

At the same time, the payment network sends a message back to the originating bank with the details of the payment and the amount of the currency conversion.

The originating bank then sends the funds from the sender's account to the payment network, and the payment network credits the funds to the recipient's bank in the destination country. When the funds are received, the recipient's bank informs the recipient of the payment, and the funds are available for use.

In an ecommerce context, cross-border payments work much the same. However, they are typically facilitated through a payment gateway, which acts as a bridge between the business and the payment processor. A customer's payment information is secured via a checkout page and transmitted to the payment processor, which initiates the payment transaction.

Once the payment is approved, the payment processor sends a confirmation to the business and the customer. The customer will usually receive a receipt for their purchase, and the merchant will receive notification of the sale. The business will then be able to transfer the funds to its account.

Examples of Cross-Border Payment Methods

Cross-border payments can be made through a variety of different payment methods. A wire transfer is an electronic funds transfer from one bank account to another internationally. A wire transfer requires the sender to provide the recipient’s bank details, such as their name, account number and routing number. The money is then transferred from the sender’s bank account to the recipient’s bank account.

Credit/debit card payments are one of the most popular methods for making cross-border payments. The sender simply needs to provide the card details of the recipient, such as their name, card number, expiry date, and security code. The payment is then processed and the money is transferred from the sender’s card to the recipient’s card.

Money transfer services are online money transfer platforms that allow you to send money from one country to another. All that’s needed to complete a cross-border payment is to provide the recipient’s name, address, and bank details. The money is then transferred from the sender’s account to the recipient’s account.

Digital wallets are electronic, digital versions of traditional physical wallets. Many offer cross-border payment services. Users simply need to enter their payment information and select the country they are sending money. The digital wallet will then convert the funds into the currency of the recipient’s country and transfer the money.

Why Are Cross-Border Payments Important for Businesses?

Cross-border payments are important for businesses because they allow you to operate in an increasingly globalized world. In today’s business environment, the ability to quickly and securely send payments to suppliers and customers in other countries is absolutely essential.

Cross-border payments also allow businesses to expand their customer base by enabling them to accept payments in multiple currencies from customers around the world. This makes it easier for your business to process orders from international customers, opening up new markets and opportunities for growth. This is especially beneficial for businesses looking to scale up their operations.

The Challenges of Accepting Cross-Border Payments

Accepting cross-border payments can be a complicated and challenging process for businesses due to a number of factors. These include:

1. Currency Conversion

One of the biggest challenges of accepting cross-border payments is dealing with multiple currencies. Businesses must manage the risk of fluctuating exchange rates and be aware of fees associated with currency conversion which can reduce profits and increase operational costs.

2. Compliance

Different countries can have different regulations and laws that govern international payments, which makes it difficult to ensure that all payments are compliant. Depending on the countries involved, specific compliance requirements may need to be met before a payment can be accepted.

These include Know Your Customer (KYC) regulations, Anti-Money Laundering (AML) requirements, and other legal regulations. There may also be restrictions on what kind of payments can be made in certain countries, which can limit your business’s ability to accept payments.

3. Payment Processing

Another challenge of accepting cross-border payments is the complexity of payment processing. Cross-border payments typically require multiple steps and regulations that need to be followed in order to successfully transfer money from one country to another.

They can involve multiple parties, such as banks, payment processors, and financial networks. This can make it difficult to ensure payments are processed quickly and securely, leading to customer frustration if payments are rejected or slow.

4. Payment Methods

Customers in different countries have different payment preferences and requirements, so offering multiple local payment methods is critical to reduce the risk of failed payments and make the checkout process easier and more efficient.

However, providing a wide range of local payment options requires businesses to have the necessary infrastructure in place. This can often require significant time and resources to set up and can be costly without the right payment service provider.

5. Fraud Prevention

Cross-border payments are vulnerable to fraud as the complex nature of international payment processing provides more opportunities for fraudsters to exploit.

Cross-border payments involve different players, currencies, and jurisdictions and require more coordination between these parties, making it more difficult to detect and deter fraud. It's critical for businesses to have strong fraud prevention standards and protections in place to safeguard against this threat.

The Benefits of Using Pay.com as Your Payment Service Provider

Pay.com offers many advantages to your business, making it the perfect payment partner. You can easily accept credit and debit cards and a variety of other payment methods from domestic and international customers and quickly integrate new ones in a few clicks through the Pay Dashboard.

Pay.com has the highest level of security compliance with Level 1 PCI DSS. This is maintained through regular auditing and testing. You can show the PCI DSS logo on your checkout page to demonstrate your security commitment to customers.

Pay.com uses secure tokenization to protect data in transit, reducing the chance of a hostile actor intercepting sensitive information from your customers. All credit card information from customers is tokenized and card numbers are never retained on our servers.

Pay.com also supports 3D Secure 2.0 (3DS2) which provides an additional layer of authentication and protection. With 3DS2, your business and its customers can be confident that payments are safe and secure.

Getting set up is quick and painless. Pay.com's developer-friendly APIs make it simple for your developers to integrate secure payment processing and management capabilities.

The Pay Dashboard is user-friendly, allowing your team to manage all aspects of payments in one place. This covers capabilities such as adding new payment methods and checking the status of all your payments, as well as updating customer information, issuing full or partial refunds, and viewing detailed reports and analytics.

Click here to get started with Pay.com now!

The Bottom Line

Global business opportunities are waiting to be explored, but the complexities of cross-border payments can make them a daunting prospect. Fortunately, with the right knowledge and the right partner, such payments can be a smooth and stress-free experience.

Pay.com provides the full payment infrastructure you need to accept cross-border payments, making it easier than ever to take advantage of global opportunities and grow your customer base.

With Pay.com, you can expand your business without having to worry about the additional risks and costs that come with cross-border payments. Click here to create your account now!

Pay.com makes it easy for your business to accept credit cards and a wide variety of other payment methods from customers in different countries. You can easily track all your cross-border payments and fees and don’t have to worry about any nasty surprises at the end of the month.

Read next

Get payments insights in your inbox