Business Inventory Management: The Ultimate Guide for 2026

8 min read

•

24 Feb 2026

It’s not exactly a well-kept secret that inventory management is one of the most critical parts of operating a successful business. Yet many ecommerce merchants continue to overlook the importance of managing inventory and fail to comprehend how it can impact their business. A recent report by GT Nexus found that worldwide losses from mismanaged inventory were $1.75 trillion! Pretty crazy, right? Simply doing the bare minimum or neglecting inventory management altogether, even for small businesses, is a recipe for disaster. With that said, let’s take a look at what inventory management actually is, why it's so important and the systems, techniques and methods you can use to do it effectively.

Inventory management definition

Inventory management is the process of keeping track of the products that are being purchased, sold, or used in a business. It’s usually done with the help of an inventory management system that helps record and track the inventory levels, sales, and purchases.

Types of inventory

There are four common types of inventory:

- Raw materials: These include the materials used to produce finished products.

- Work in Progress (WIP): Work-in-progress inventory refers to the raw materials that are in the process of being made into a product.

- Maintenance, Repair, and Operating Supplies (MRO): These are items needed to support the production of a product but are not included as a part of the finished product. Examples include things like safety equipment, cleaning supplies, packaging materials and computers.

- Finished goods: These are simply goods or products that are complete and ready to be sold.

Are stock and inventory the same thing?

The terms inventory and stock often get used interchangeably. However, there is a slight difference between the two. Inventory refers to the finished products you sell to customers and the materials, equipment and supplies needed to create this product. On the other hand, stock refers to the finished products currently available to sell to customers.

Why is inventory management important?

Keeping a close eye on your inventory is essential to run your business smoothly. Here are the main benefits.

Keep customers happy

Consumers and businesses have high expectations and more choices than ever before in today’s global and on-demand world. Effective inventory management can help you meet these rising expectations and keep your customers satisfied by solidifying your business’ ability to fulfill orders and deliver products faster. If your business is out of stock, slow to deliver, or sends the wrong item, a customer will likely not make another purchase in the future. So, in other words, effective inventory management can help you avoid these situations and keep your customers loyal and happy!

Increase productivity

Effectively managing your inventory enables you to gain greater control over your costs and boost productivity by reducing errors and the need for time-consuming

manual input to track inventory. By doing so, you can invest more time and resources into other areas of your business.

Increase productivity

Effectively managing your inventory enables you to gain greater control over your costs and boost productivity by reducing errors and the need for time-consuming manual input to track inventory. By doing so, you can invest more time and resources into other areas of your business.

Reduce costs

Conducting effective inventory management enables your business to understand what products are top sellers, what’s not selling well, which are running low, and understand what items are already stocked. This can help you avoid problems such as overstocking, which can quickly add to your business’s costs and lead to losses, especially when too much inventory is purchased that cannot be sold. There are also additional storage costs that stem from overstocking, which can be avoided.

Support growth

While many smaller online businesses may settle for a more manual, ad-hoc approach to inventory management, this can inhibit growth. The reality is, the larger the company, the more critical inventory management becomes. With effective inventory management processes and systems in place, businesses can quickly respond to increased demand, add new product lines, and grow.

Why do you need an inventory management system?

An inventory management system helps your business manage its inventory in a more organised and efficient manner. Without a well-designed system in place, you’ll be working blind, with little structure or direction, and on an ad-hoc basis

which will quickly lead to big problems that can severely impact your operations. You’ll start to have too much inventory or not enough, and you will waste money

purchasing inventory you don’t need. Either way, your reputation, and profits will take a hit. This is especially true for larger businesses with lots of different product lines and product components.

What is the first step of inventory management?

The first step in inventory management is to decide which system you will use to record and track inventory. Whether that be a spreadsheet or specialised software, the system you choose depends on the size of your business and its unique requirements in terms of the types of products you sell and product data that needs to be tracked. After you have decided on which inventory management system to use, you’ll need to record your current inventory levels and then begin forecasting customer demand by looking at sales data to determine how much inventory you require in the future.

How to do inventory management

There is no “one size fits all” way to do inventory management. There are simply too many variables like the size of a business, number of products sold, and budget, amongst others. That said, there are a few key inventory management techniques every business should practice.

Get the right software system in place

Even though many smaller merchants continue to use excel to track their inventory, using specialised software can save you time, money, and a lot of stress in the long run. Specialist software can also automate some inventory management tasks, helping to support your business’s growth, unlike excel, which can become a nightmare as you scale your operations.

Conduct regular audits

Whether using an expensive specialised software system or a simple Excel spreadsheet to manage your inventory, conducting regular inventory audits is a

must. An audit is a manual check of the quantities and condition of the current inventory in your possession. Audits are done to ensure the inventory quantities

match what you have recorded in your management system. Audits are critical because it helps you find any discrepancies and track any theft that may have occurred. Moreover, audits also help you find damaged stock and identify any items that are not selling or overstocked.

Set reorder point or par levels

Setting reorder points can save your business a lot of problems and stress. Put simply, a reorder point is the absolute minimum amount of each stock you need to have to avoid running out. When inventory levels reach a reorder point, you know it’s time to order more inventory. To calculate your reorder point, you’ll need to use the following formula:

Daily unit sales X Lead time + Safety stock

If we break these terms down:

- Daily unit sales is the average of how much of a certain product you sell each day.

- Lead time refers to how much time it takes for new inventory to arrive once you’ve reordered it.

- Safety stock is the additional stock you keep on hand in case of errors or delays.

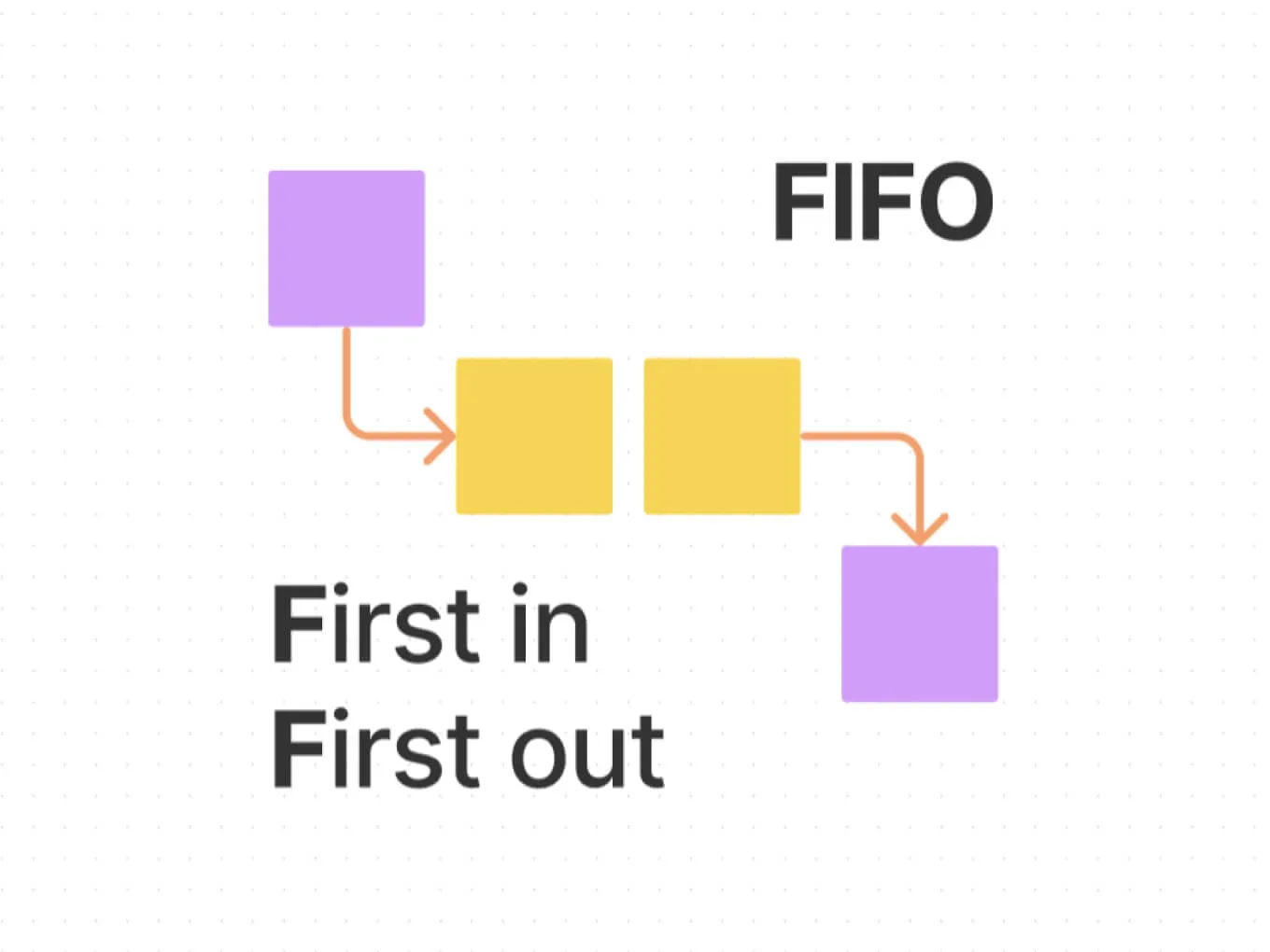

Utilise the “First In First Out” (FIFO) approach

First In First Out, aka FIFO, is a widely used accounting and valuation method to control and determine the cost of inventory. Understanding and using the FIFO method is vital because the purchase price of inventory changes over time due to

fluctuating raw material costs and exchange rates, making it harder for businesses to understand their profits levels. The FIFO method is logical and straightforward as it

follows the view that the oldest stock is usually sold first, which makes calculating profits and updating financial statements easier and faster.

How to use Excel and create a business inventory management system

It’s common for smaller businesses to use Excel when getting started with inventory management because it’s fast and low-cost. However, if your business grows and introduces new products, Excel can become challenging to manage, and minor human errors can turn into costly problems. With that said, if you want to use Excel to manage inventory, the program provides numerous ways to list and categorise data as well as formulas for calculations. Ultimately, the most challenging part of using excel isn’t actually using the program itself. Instead, it’s working out what to track and how to categorise your data. The excellent news with Excel is that if building your own spreadsheet is too tricky, the program enables you to choose from a range of templates explicitly created for inventory management.

Which is not a primary goal of inventory management?

Despite what is commonly believed, the primary goal of inventory management is not to obtain the lowest cost of inventory. It also isn’t to keep a large inventory for long periods of time. Instead, the primary goal of inventory management is to maintain inventory at optimal levels to avoid shortages and excesses.

Inventory management analysis

A lot of time, money, and energy is spent on managing inventory. It’s essential to track KPIs to ensure these efforts are effective. KPIs are the measures of performance that allow you to gauge the overall success of your inventory management team’s efforts. Here are a few major indicators every merchant needs to track.

Turnover rate

Inventory turnover rate shows the number of times inventory was sold and replaced during a specific period. Your turnover rate lets you know how fast you’re selling your inventory. Formula: Inventory turnover rate = cost of goods sold / average inventory

Stock to Sales Ratio

The stock to sales ratio shows the stock available for sale against the stock already sold. The ratio is a great way to ensure your inventory is always kept at the optimal level. Formula: inventory value ÷ sales value

Days on Hand

Weeks on hand shows the average amount of time inventory turns over each day. It gives you an indication of how fast your inventory is turning over. Formula: Average inventory/cost of sales x 365

Weeks on Hand

Weeks on hand shows the average amount of time it takes to sell inventory each week. It gives you an indication of how fast your inventory is turning over. Formula: Average inventory/cost of sales x 52

Sell Through Rate

Sell through rate shows you the percentage of units in your current inventory sold during a specific period. Formula: Number of units sold / Number units received x 100

Back Order Rate

Back order rate measures the level at which your inventory is meeting customer demands. Formula: Number of delayed orders due to backorders / total number of orders placed) x 100

Time to Receive

This KPI is all about measuring how efficient your business is at receiving inventory and preparing it for sale. Formula: Time needed for inventory validation + time to add inventory into records + time to put inventory into storage

Put Away Time

Put Away Time refers to the total time it takes to put away or store inventory. Formula: Total time to put away inventory

Inventory management methods (Examples)

Just-in-Time Management (JIT)

Just-in-Time is an inventory management method that makes the stock needed, when it’s needed, in the quantity that’s required. Using this method enables businesses to only keep the minimum amount of inventory on hand. When stock is sold, an immediate reorder occurs to replace stock that has just sold.

Materials requirement planning (MRP)

MRP is a method for calculating the materials and components needed to make a product. MRP involves:

- checking current inventory levels

- pinpointing which materials are required

- scheduling when to purchase these materials

Economic Order Quantity (EOQ)

The economic order quantity (EOQ) method is based on the view that businesses should purchase the precise inventory to minimize storage, order and other associated costs. The formula to calculate EOQ is as follows: EOQ = square root of 2 x Setup costs x Demand rate/holding costs.

Read next

Get payments insights in your inbox